Solution (a) direct methodThe direct method is relatively straightforward in that all the data are cash flows so it is a case of listing the receipts as positive and the payments as negative. For each movement in working capital, you must consider whether it has had a favourable or unfavourable cash flow impact on the business. If the impact is favourable, then the movement in the year should be added on to profit before tax as part of the reconciliation. The Statement of Financial Accounting Standards No. 95 encourages use of the direct method but permits use of the indirect method. Whenever given a choice between the indirect and direct methods in similar situations, accountants choose the indirect method almost exclusively.

AccountingTools

However, surveys indicate that nearly all large U.S. corporations use the indirect method. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. EXAMPLE 2 – Calculating the payments to buy PPEAt 1 January 20X1, Crombie Co had PPE with a carrying amount of $10,000. During the year, depreciation charged was $2,000, a revaluation surplus of $6,000 was recorded and PPE with a carrying amount of $1,500 was sold for $2,000. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license.

Cash flow statements

When added to the opening cash balance of $250,000, the resulting total of $307,500 is equal to the ending cash balance for the year ending December 31, 2020. This can be seen in the completed statement of cash flows following step 8. Note that the cash proceeds from the disposal of PPE ($2,000) would be shown separately as a positive cash inflow under investing activities. The profit on disposal of PPE of $500 ($2,000 – $1,500) would be adjusted for as a non-cash item under the operating activities (see later). Deprecation reduces the carrying amount of the PPE without being a cash flow. The double entry for depreciation is a debit to statement of profit or loss to reflect the expense and to credit the asset to reflect its consumption.

2: Direct and Indirect Methods for Preparing a Statement of Cash Flows

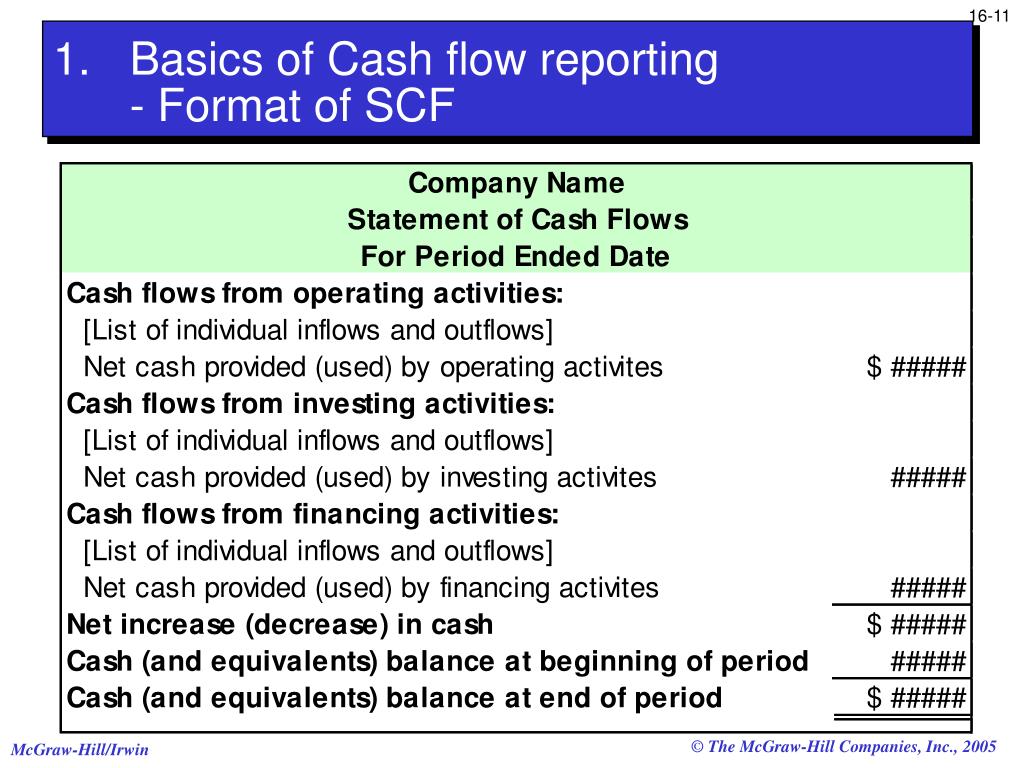

- The profit before tax is then reconciled to the cash that it has generated.

- This transaction has no effect on cash and, therefore, should not be included when measuring cash from operations.

- This means that the figures at the start of the cash flow statement are not cash flows at all.

- Both the direct and indirect methods of preparing a statement of cash flows will be addressed in this article.

- Examples of cash flows from financing activities include the cash received from new borrowings or the cash repayment of debt.

Moreover, the transactions resulting in cash inflows are to be differentiated from the transactions resulting in cash outflows for each account. Preparing a statement of cash flows is made much easier if specific the reporting of investing activities is identical under the direct method and indirect method. sequential steps are followed. For instance, the net cash flows from operating activities is the same for both methods, and the investing and financing activities are identical for both methods as well.

Computing cash flows

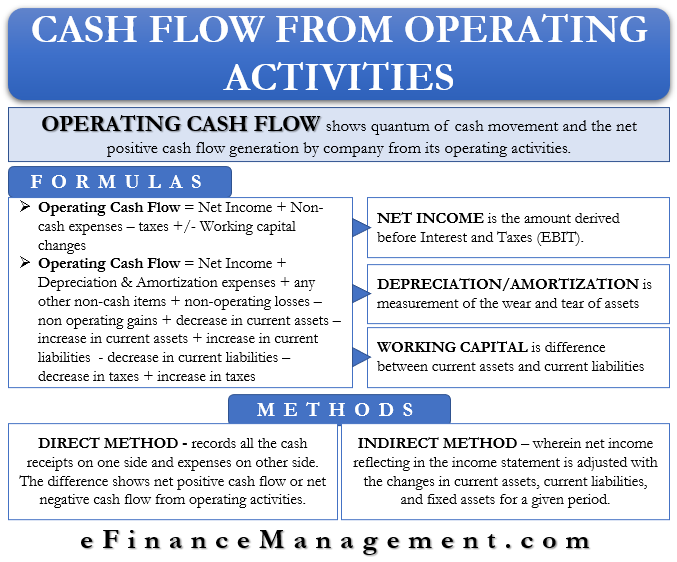

Enter the amount of the net income/(loss) as the first amount in the operating activities section. Next, review the income statement and select all the non-cash items. Look for items such as depreciation, depletion, amortization, and gains or losses (such as with the sale or disposal of assets). In this case, there are two non-cash items to adjust from net income. Record them as adjustments to net income in the statement of cash flows.

For example, the statement may include line items for changes in the ending balance of accounts receivable, inventory, and accounts payable. The intent is to convert the entity’s net income derived under the accrual basis of accounting to cash flows from operating activities. Quick shows the $9,000 inflow from the sale of the equipment on its statement of cash flows as a cash inflow from investing activities. Thus, it has already recognized the total $9,000 effect on cash (including the $2,000 gain) as resulting from an investing activity. Since the $2,000 gain is also included in calculating net income, Quick must deduct the gain in converting net income to cash flows from operating activities to avoid double-counting the gain.

This rate of return is known as the discounted rate, which is essentially the interest rate, discounted over some time. The expected cash flows are discounted at a discount rate to compute the present value. The higher the discount rate, the higher the future value (FV), but the lower the present value.

The statement of cash flows using the indirect method has been discussed in most introductory accounting courses. Since the statement of cash flows can be challenging, a review of the basic concepts is presented below. The indirect method works from net income, so the bottom of the income statement, and adjusts it to the cash basis. We will look at both methods with the same data, so you can see the differences in analysis, but the same ending number. The direct method, the income statement is reformulated on a cash basis, rather than an accrual basis from the top of the statement (the income part) to the bottom (the expense part). Companies may add other expenses and losses back to net income because they do not actually use company cash in addition to depreciation.

本站尊重原创,素材来源于网络,好的内容值得分享,如有侵权请及时联系我们给予删除!

微信扫一扫

微信扫一扫  支付宝扫一扫

支付宝扫一扫

{kind=link}